The Growing Information Gap – June 2026

Click here to download a PDF version of The Growing Information Gap.

One of the most important shifts in investing over the last decade has received surprisingly little attention.

It is not artificial intelligence, passive investing, or the concentration of market returns among a handful of mega-cap stocks. It is the steady decline of sell-side research.

For decades, investors benefited from a large research ecosystem. Analysts built models, met with management teams, published research, and continuously updated earnings estimates. The system was imperfect, but it created a broad foundation of information that helped markets function efficiently.

That foundation has been shrinking.

Since 2018, global spending on equity research has fallen by roughly 50%. At many major banks, research headcount has declined by more than 30% over the past decade. Coverage has become increasingly concentrated in the largest companies, leaving much of the small and mid-cap universe with fewer resources devoted to understanding their businesses. Today, nearly 97% of S&P 500® companies have at least ten analyst ratings, while the number of Russell 2000® companies with fewer than ten recommendations has increased by roughly 70% over the last decade.

For active investors, that matters.

Markets are generally most efficient where information is abundant. When dozens of analysts follow the same company, it becomes increasingly difficult to uncover information that is not already reflected in the stock price. The opposite is often true when coverage is limited.

As research resources decline, information gaps emerge. Estimates become less accurate, important developments take longer to reach consensus expectations, and earnings discrepancies become more common.

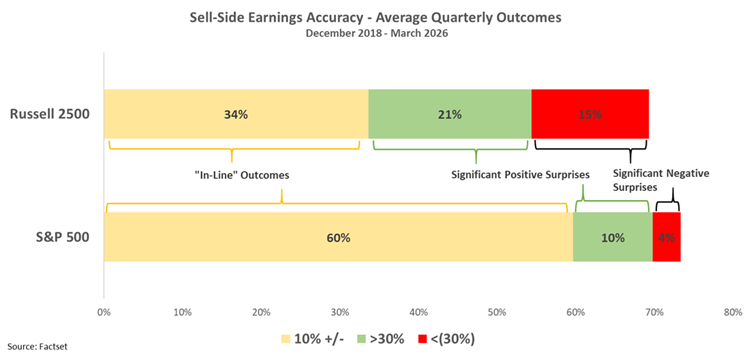

The evidence can be seen in earnings outcomes. At the end of 2018, 43% of Russell 2500® companies reported earnings within 10% of consensus expectations, compared to 65% of S&P 500 companies. At the other end of the spectrum, 29% of Russell 2500 companies reported results that differed from estimates by more than 30%, versus just 9% of S&P 500 companies. Since then, companies in the Russell 2500 reporting earnings within 10% of expectations has declined to an average of 34%, while 36% have differed by more than 30%. For the S&P 500, those figures are 60% and 14%, respectively.

The takeaway is straightforward: consensus estimates become less reliable as you move away from the largest and most heavily followed companies.

For active investors, we believe those forecasting errors are often where opportunity begins.

Stock prices react not to absolute results, but to the difference between reported results and investor expectations. When expectations are materially wrong, whether too high or too low, the resulting price moves can be significant. In our view, identifying those disconnects before they appear in reported earnings is one reason deep fundamental research remains valuable.

Management meetings, conversations with customers and suppliers, discussions with competitors, and ongoing industry work are ultimately attempts to answer a simple question: what is the market missing? In an environment where consensus estimates are becoming less accurate across much of the small and mid-cap universe, answering that question correctly can create a meaningful advantage.

We see evidence of this repeatedly. A company executes better than expected, demand proves stronger than anticipated, or margins improve faster than consensus forecasts suggest. Analysts revise estimates higher and the market adjusts accordingly.

The market often views these developments as earnings surprises. More often, they are simply examples of reality diverging from expectations.

That distinction matters.

Stock prices do not move solely because businesses grow. They move because results differ from what investors expected. When expectations are wrong, prices eventually adjust.

Ironically, the same forces that have fueled passive investing may be increasing the importance of fundamental research in certain market segments. As passive assets continue to grow and traditional research resources continue to shrink, fewer market participants are performing the deep fundamental work required to understand individual businesses.

That does not guarantee opportunity. It does, however, increase the value of independent research.

The opportunity today is not simply finding good companies. It is finding businesses where expectations do not fully reflect reality.

As sell-side research contracts and investor attention becomes increasingly concentrated among the largest stocks, the information gap across smaller and less-followed companies continues to widen. For investors willing to do the work, that gap can create meaningful opportunity.

Markets are still competitive. Information still matters.

The difference today is that fewer people are doing the work required to uncover it.

Sources: FactSet, Bloomberg. Past performance does not guarantee future results. Information has been gathered from sources considered to be reliable, however its accuracy cannot be guaranteed. All investing involves risk, including risk of loss. This material is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Opinions expressed are current as of the date of publication and are subject to change without notice.